They say there’s no such thing as a free lunch, but what about a tax-deductible lunch? While many of your income sources can be taxed, there are strategies to minimize your overall tax burden before and in retirement. One of the advantages of going to one professional for all of your financial planning needs is that everything from investment strategies to Social Security Maximization to income planning works together in one overall plan. Some advisors can also consider your tax burden in each of these areas, and work to make your financial plan more tax efficient. Here are 3 ways a financial advisor can help you through tax strategies.

Manage Investments with a Tax-Smart Strategy

Every part of a financial plan is connected, including an investment strategy and a tax minimization strategy. A good advisor invests with tax implications in mind. It’s important to factor in your tax burden when realizing investment gains, selling property, and withdrawing from a traditional IRA or 401(k). There are many tax minimization strategies an advisor can help you consider, each unique to your individual situation. Unlike an accountant who tries to reduce your tax burden on a year to year basis, an advisor can help you create a long-term tax minimization plan that lasts throughout retirement.

Social Security Maximization

If you’ve paid into Social Security for decades, you probably want to get the greatest possible amount out of it. There are so many ways to claim, and the right strategy depends on the individual. Taxes are also a concern, as 50%, or even 85% of your benefit may be taxable, depending on your income level. A financial advisor can learn about your unique situation from both a financial and lifestyle standpoint, and help you make the optimal decision. Those who are working while taking Social Security, want to claim spousal benefits, or are concerned about taxes on their benefit may have questions that an advisor can answer.

Using Retirement Accounts

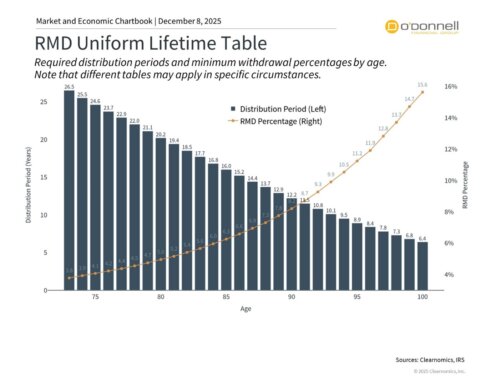

If you’ve saved a substantial amount in your 401(k), IRA, or other retirement account, it’s important to have a withdrawal strategy. Deciding how much to contribute, which kind of plan is best for you, when to start withdrawing, and whether to utilize a Roth IRA are all important decisions a financial advisor can help you make. Starting at age 72, you will mostly likely have to take Required Minimum Distributions (RMDs) from your traditional retirement plans. This can cause you to withdraw more than you want to in a year, potentially increasing your tax burden. When it comes to taxes, plan for your future self. This includes having a strategy for taking RMDs.

At O’Donnell Financial Group, we can help you fit all the pieces of the puzzle together with an income and tax-minimization plan. We can help you figure out which income sources to draw on and when, how new sources of income could affect your tax burden, and how to help reduce taxes on your heirs. Click here to sign up for a complimentary review where we can assess your tax burden.