Retirement is a major event that can drastically change your day-to-day life, your financial strategies, and even your tax burden. Retirees may no longer receive taxable income from an employer, but they will likely receive income from other sources which can be taxed. This is why when it comes to taxes, it’s important to help plan for your future self.

Now vs. Tomorrow

Right now, many people are enjoying relatively low tax rates: In 1944 the highest income tax rate was 94%, and in 1978 the maximum capital gains tax rate was almost 40%.1 Currently, the highest income tax bracket is 37% and the highest long-term capital gains tax rate is 20%. 2 With a growing national debt and leadership in Washington always subject to change, it can be hard to predict what tax rates will look like in 10, 20, and 30 or more years into the future. That’s why it’s important to have a plan to help minimize your taxes in retirement.

Social Security

To help determine if you will owe tax on your Social Security benefit, add up your adjusted gross income, nontaxable interest, and half of your Social Security benefit. If it’s more than $25,000 as an individual, or more than $32,000 if you’re married and filing jointly, then you will likely owe tax on up to 50% of your benefit. As a single filer, if your combined income is more than $34,000, or as a married couple filing jointly with combined income over $44,000, then up to 85% of your benefit can be taxed.3 This is why integrating a Social Security maximization strategy with an overall plan to help minimize your tax burden in retirement is vital when planning for your future self.

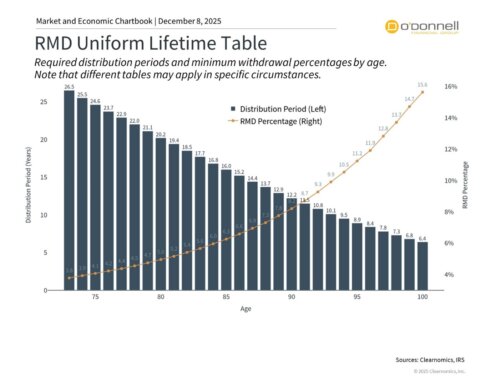

Retirement Account Distributions

If you have a traditional 401(k) or IRA, you will transition from enjoying their tax-deferred status to paying taxes on distributions in retirement. Even if you don’t need the money right away, you will eventually have to start withdrawing from them annually after you turn age 70 ½. Distributions from Roth accounts however, are not taxed because they are funded with after-tax dollars. One tax minimization strategy to consider is to convert funds from traditional retirement accounts such as 401(k)s and IRAs to a Roth account. In this case you would pay tax on the amount converted at today’s rates, rather than pay the unknown rates of the future on distributions from a traditional retirement account.

Investment Sales

You might sell an investment in retirement, and that sale can trigger a capital gains tax. Investments held for under a year are taxed at regular income-tax rates, but investments held for over a year are taxed at the preferential rates of 15% and 20%. And, long-term capital gains are not taxed if your income as a couple is under $78,750 or under $39,375 as single filer.4

Here at O’Donnell Financial Group, we can help you plan for the long-term by assessing your current situation and potential future tax burden in retirement. Taxes don’t disappear in retirement, so plan for your future self. We offer complimentary financial reviews so that you can get your questions answered, and we can help you take the first step towards creating a comprehensive retirement plan built to last for the long road ahead.