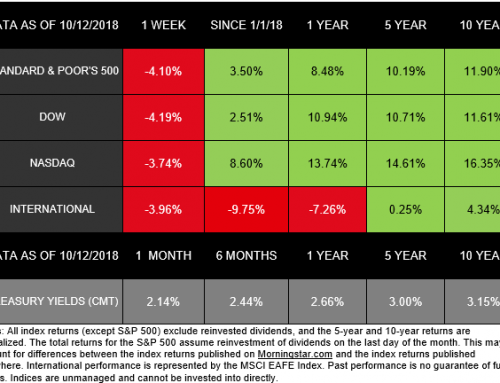

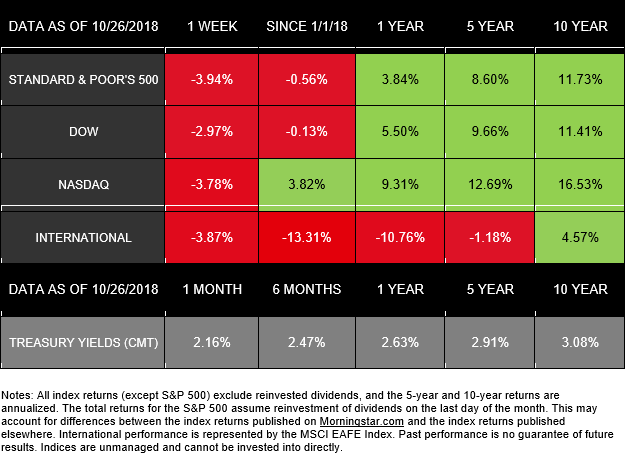

Last week did nothing to dispel October’s reputation as a tough month for the markets. The S&P 500 lost 3.94%, the Dow declined 2.97%, and the NASDAQ dropped 3.78% during what was one of 2018’s most volatile weeks so far. All three indexes are down significantly for the month, and both the S&P 500 and Dow have entered negative territory for 2018.[i] International stocks in the MSCI EAFE also struggled, posting a 3.87% drop for the week, and a 13.31% decline for the year.[ii]

Why did stocks drop? Will they continue to do so?

Currently, many topics are on investors’ minds, from inflation to tariffs to valuations and beyond, but analysts are not pointing to one single culprit for last week’s performance. Instead, a mixture of concerns, with a large dose of emotion, seemed to drive the markets.[iii]

Emotional reactions are understandable when volatility emerges, but they have no place in long-term investment strategies. Instead, we need to focus on the fundamentals.

What did we learn last week?

Trying to find simple explanations for market behavior can feel impossible, in part because the markets aren’t a machine¾they’re a reflection of many human actions. Investors make choices based on their interpretations of current conditions, and the effects of these decisions become “market performance.”

Amidst the volatility, we received several updates on the economy, including:

- 3rd Quarter Gross Domestic Product (GDP) beat expectations: The initial GDP reading for the 3rd quarter came in at a strong 3.5%, helped in large part by consumer spending.[iv]

- Corporate earnings have been strong, but imperfect: So far, this corporate earnings season is showing 22% growth, but fewer S&P 500 companies are exceeding analysts’ predictions than in the 1st quarter of 2018. In particular, some major tech companies’ results disappointed investors.[v]

- Housing continued to struggle: New home sales were lower than expected in September, which followed disappointing results from existing-home sales data, as well.[vi]

- Inflation growth eased: The Personal Consumption Expenditures Price Index, which shows inflation, increased by 1.6% in the 3rd quarter, much lower than projected.[vii]

Examined together, this data indicates that while the economy has potential challenges, it also demonstrates solid growth, reasonable inflation, and strong corporate performance. That story feels different than the sharp drop we experienced last week. However, when you look at the bigger picture, our current circumstances provide another reminder that volatility is normal, and examining economic fundamentals is critical.

Still, risks exist, and in the coming weeks we will pay very close attention to data and performance. In particular, we will follow the Federal Reserve’s comments and actions to see what may lie ahead for interest rates. In the meantime, please let us help answer your questions and address your concerns. We are here to help you pursue your goals, in every market environment.

ECONOMIC CALENDAR

Monday: Personal Income and Outlays

Tuesday: Consumer Confidence

Wednesday: ADP Employment Report

Thursday: PMI Manufacturing Index, ISM Manufacturing Index, Construction Spending, Jobless Claims

Friday: Employment Situation, Factory Orders

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.