The Week on Wall Street

An open-ended commitment by the Federal Reserve to support American businesses and capital markets along with the passage of a $2 trillion aid package improved investor sentiment and drove a strong rally in stock prices.

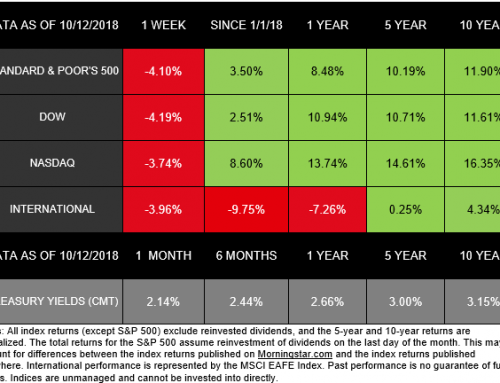

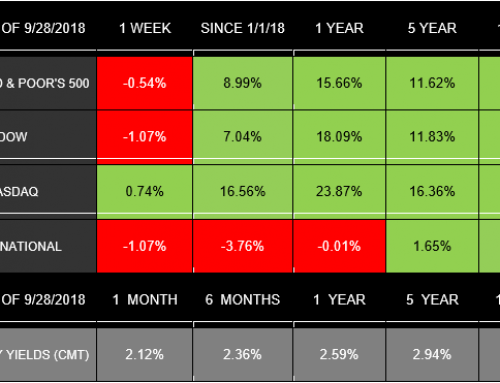

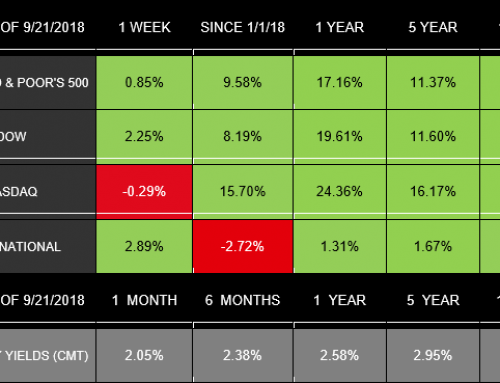

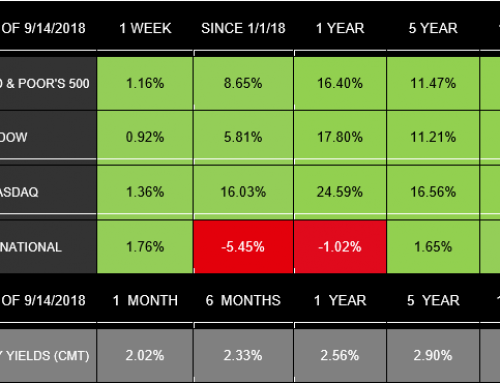

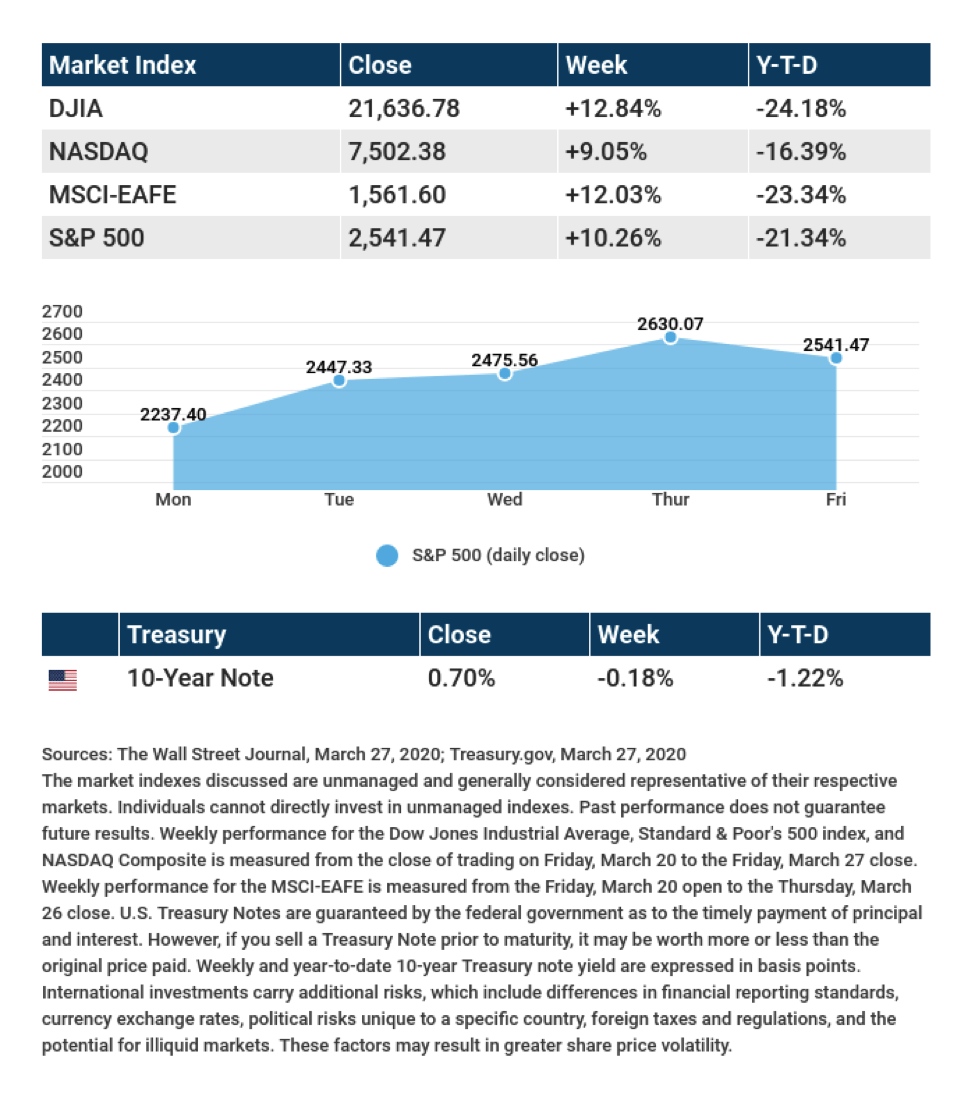

The Dow Jones Industrial Average jumped 12.84%, while the Standard & Poor’s 500 gained 10.26%. The Nasdaq Composite index rose 9.05% for the week. The MSCI EAFE index, which tracks developed overseas stock markets, increased by 12.03%.[i],[ii],[iii]

Stocks Rebound

A stunning string of Federal Reserve initiatives and the passage of a $2 trillion aid bill buoyed stocks this week, with the Dow Jones Industrial Average jumping by over 11% on Tuesday, its best day since 1933. Stocks continued to strengthen the following day, registering their first back-to-back gains since February.[iv],[v]

Despite a record 3.28 million jobless claims, stocks added to their gains for a third straight day. Stocks gave back some gains on the final day of trading to end an otherwise welcomed week of positive price action.[vi]

A Shift in the Conversation

The conversation around the domestic spread of the coronavirus has been centered on “flattening the curve,” with closures of local businesses and schools, a shift to working from home, and appeals for social distancing.

Hitting the pause button on the U.S. economy, however, has had its consequences, including massive job losses, sharp declines in business revenues, and disarray in the capital markets. This week the conversation shifted to include how to restart the economy amid a pandemic that may not have yet peaked.

Final Thought

On a strictly definitional basis, the three-day surge in stock indices this week signaled a new bull market (when stocks rise 20% after having fallen 20% or more). But it’s hard for even professional investors to make sense of a market that enters a bear market and a bull market in the same month. This volatility certainly speaks to the deep health and economic uncertainties that exist.

It’s not clear what the rally this past week means for the market going forward. Absent such clarity, markets are likely to remain volatile in the near term, requiring investors to be patient with their long-term investments and wait as calmly as possible for time to answer the big questions overhanging today’s market.

THE WEEK AHEAD: KEY ECONOMIC DATA

Tuesday: Consumer Confidence.

Wednesday: Automated Data Processing (ADP) Employment Report. Purchasing Managers Index (PMI): Manufacturing Index. Institute for Supply Management (ISM) Manufacturing Index.

Thursday: Jobless Claims for Unemployment. Factory Orders.

Friday: Employment Situation Report. Purchasing Managers Index (PMI): Services Index.

Source: Econoday, March 27, 2020

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

THE WEEK AHEAD: COMPANIES REPORTING EARNINGS

Tuesday: Conagra Brands (CAG), McCormick & Co. (MKC)

Thursday: Walgreens Boots (WBA), Chewy (CHWY)

Friday: Constellation Brands (STZ)

Source: Zacks, March 27, 2020

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Any investment should be consistent with your objectives, time frame and risk tolerance. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Diversification does not guarantee profit nor is it guaranteed to protect assets. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. The DJIA was invented by Charles Dow back in 1896.

The Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of stocks of technology companies and growth companies.

The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indices from Europe, Australia, and Southeast Asia.

The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-COMPLIMENTARY borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Past performance does not guarantee future results.

You cannot invest directly in an index.

Consult your financial professional before making any investment decision.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

These are the views of Platinum Advisor Strategies, LLC, and not necessarily those of the named representative, Broker dealer or Investment Advisor, and should not be construed as investment advice. Neither the named representative nor the named Broker dealer or Investment Advisor gives tax or legal advice. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor for further information.

By clicking on these links, you will leave our server, as the links are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[i] The Wall Street Journal, March 27, 2020.

[ii] The Wall Street Journal, March 27, 2020.

[iii] The Wall Street Journal, March 27, 2020.

[iv] CNBC.com, March 23, 2020.

[v] The Wall Street Journal, March 25, 2020.

[vi] The Wall Street Journal, March 26, 2020.